Imagine spending decades saving, investing in property, and planning for a secure retirement, only to see your nest egg disappear due to long-term care costs or nursing home expenses. This is a growing concern for many retirees, especially with Medicaid’s strict eligibility limits.

So, can a trust protect your assets from Medicaid? This guide explains how trusts work in Medicaid planning, the types available, and how to set one up to safeguard your financial legacy.

Medicaid is a government program that provides long-term care assistance, but it’s income and asset-tested. To qualify, you must have minimal countable assets. However, by using a Medicaid-compliant trust, certain assets can be legally excluded from consideration, helping you preserve your wealth while qualifying for benefits.

This approach is known as Medicaid asset protection planning, a legitimate and proactive financial strategy often used in estate planning.

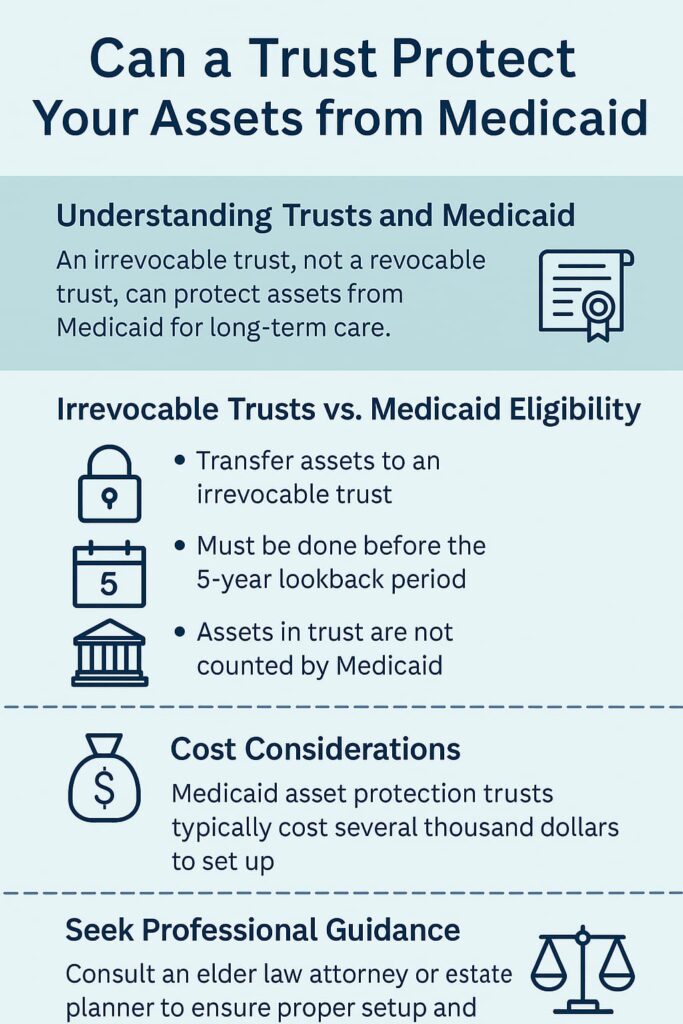

An irrevocable trust is one of the most reliable tools for shielding assets from Medicaid eligibility reviews. Once you transfer assets into this type of trust, they are no longer considered your personal property. Instead, the trust holds ownership, which prevents these assets from being counted against Medicaid’s financial thresholds.

Common Trusts Used in Medicaid Planning:

You may also hear terms like grantor, trustee, and beneficiary—key roles that define how the trust operates.

Jim and Carol, a retired couple with a paid-off home and moderate savings, feared losing everything to potential nursing home bills. On their attorney’s advice, they created a Medicaid Asset Protection Trust five years ago, transferring their home and bank assets into it. When Jim eventually needed care, the trust kept their assets protected. Carol maintained her lifestyle without dipping into their emergency funds.

Medicaid enforces a five-year look-back period. This means any assets transferred into a trust within five years of applying for Medicaid may result in penalties or ineligibility.

That’s why early Medicaid planning is critical. Ideally, you should begin the process well before the need for long-term care arises.

In some states, life estate deeds or Medicaid-compliant annuities may be used in tandem with trusts, depending on your goals.

1. Do Revocable Trusts Protect Assets from Medicaid?

No. Because you retain control, revocable trusts do not shield your assets from Medicaid spend-down requirements.

2. Can a Trust Protect Assets from Nursing Homes and Long-Term Care?

Yes, if structured correctly. Irrevocable trusts are often used to protect property and savings from being consumed by care costs.

3. Are Trust Assets Safe from Lawsuits or Creditors?

In most cases, yes. An irrevocable trust can provide protection from lawsuits, debt collectors, and even estate recovery actions by Medicaid.

4. Can I Still Live in My Home if It’s in a Trust?

Yes. With proper structuring, you can retain the right to live in your home while it’s held in the trust.

5. What About Spousal Protections?

Spousal refusal or community spouse rules can work alongside trusts to protect one spouse while the other receives Medicaid benefits.

While Medicaid Asset Protection Trusts are powerful, they come with trade-offs:

Despite these drawbacks, many families find that the benefits far outweigh the limitations—especially when preserving wealth for future generations.

Step 1: Consult an Estate Planning or Elder Law Attorney

Work with a qualified professional who understands your state’s Medicaid rules. Avoid DIY templates or generic trust forms.

Step 2: Identify Which Assets to Transfer

Most commonly, this includes your home (principal residence), savings, and investment accounts.

Step 3: Choose a Trustee and Beneficiaries

This is typically a spouse, child, or trusted family member. Make sure they understand their fiduciary responsibilities.

Step 4: Execute and Fund the Trust

Your attorney will draft the trust and ensure it complies with state law. You must also transfer assets into the trust properly for it to be effective.